Design a Supermarket for Older Adults

Product Design Interview Question : Design a Supermarket that caters to Older Adults

This post is for our Paid Subscribers. If you haven’t subscribed yet,

Step 1: Ask Clarifying Questions

Before proposing a design, I want to sharpen my understanding of the problem space. A supermarket for older adults could mean very different things depending on the context.

Q: Are we designing a net-new supermarket concept from scratch, or retrofitting an existing chain such as Reliance Fresh, Spencer’s, or D-Mart for an older adult customer segment?

I will assume net-new. This lets us make intentional architectural and service decisions without being constrained by legacy store layouts or existing operational practices.

Q: What is the primary geography we are targeting? India’s urban elderly, a specific Tier 1 city, or a global audience?

India, specifically Tier 1 cities like Bengaluru, Mumbai, Delhi, and Pune, where elderly populations are growing fastest and where modern organized retail penetration is already above 30 percent. The Indian context also matters because of specific behavioral patterns: cash usage is still high among older adults, multi-generational household grocery decisions are common, and digital adoption curves differ sharply from Western markets.

Q: How do you define “older adults”? 55 and above, 65 and above, or 75 and above?

I will design for the 60 to 75 age band, often called the “active elderly.” These adults still shop independently but have emerging physical, cognitive, and social needs. Designing for 75-plus would push us toward an assistive-care model. Designing for 55-plus would blur too much into mainstream retail. The 60 to 75 band is the most underserved segment with the highest potential.

Q: Should this be a pure brick-and-mortar concept, or do we need an omnichannel model with home delivery?

Omnichannel, with the physical store as the primary experience driver. Many older adults have health episodes that prevent in-store visits. A WhatsApp or phone-based ordering channel for delivery on those days dramatically reduces churn without compromising the store’s core identity as a community gathering place.

Q: What is the business model: independent standalone store, franchise, or part of a larger retail group?

Independent concept, funded by a retail-focused impact investor or a healthcare conglomerate like Apollo or Max. This is important because it allows design choices that prioritize the customer experience over short-term margin, which is often not possible inside a large retail chain optimizing for same-store sales growth.

Q: Are there any hard constraints on store size, location type, or budget?

No hard constraints. I will assume a store of approximately 3,000 to 4,000 square feet, which is typical for a neighbourhood supermarket and large enough to include a seating area and wide aisles without becoming a hypermarket.

These clarifying questions are doing distinct work. The geography question anchors the design in Indian behavioral realities: cash prevalence, WhatsApp familiarity, and joint family dynamics. The age-band question prevents the solution from drifting toward either mainstream retail (too broad) or assistive care (too narrow). The store format question signals that you are thinking about implementation constraints, not just product ideals. Many candidates skip these and jump directly into feature lists, which produces generic answers that could describe any product for any user.

Step 2: Describe the Product

Market Context

India has approximately 140 million people aged 60 and above as of 2024, a number projected to reach 230 million by 2036, making it the fastest-growing elderly demographic in any middle-income economy. Despite this, Indian retail has almost entirely ignored this segment. Modern trade, which includes chains like Reliance Smart, Big Bazaar, and Spencer’s, optimizes entirely for speed, throughput, and impulse purchasing, not for the specific physical, cognitive, and social needs of older shoppers.

The result is that older adults either depend on family members for grocery runs, rely on traditional kirana stores with limited assortment and no quality guarantees, or endure the physical and cognitive stress of mainstream supermarkets that were never designed for them. In a survey of adults aged 60 to 75 in Mumbai and Bengaluru, 63 percent reported avoiding supermarkets during peak hours specifically because of crowding, noise, and long checkout queues. Only 19 percent said they felt “comfortable and respected” in their primary grocery store.

The Opportunity

Indian households headed by someone aged 60 and above spend an average of Rs 8,400 per month on groceries, roughly 15 percent higher than the national average, because they prioritize quality, freshness, and health over price. They are deeply brand loyal, with a 30-day churn rate estimated at under 8 percent among satisfied customers, compared to 22 percent in the general adult population. They visit grocery stores more frequently, averaging 2.4 trips per week versus 1.8 for younger cohorts. Yet no organized retail player in India has built a store specifically for them.

I propose Sankalp Fresh, a supermarket concept designed around the physical, cognitive, and social needs of adults aged 60 to 75, positioned as “India’s first supermarket that genuinely respects your time and your body.”

Competitive Landscape

There is no direct competitor in the elderly-focused grocery segment in India. The closest analogies are Japan’s Senior-Friendly Store certification programme (adopted by AEON and Ito-Yokado for stores near retirement communities) and the UK’s Sainsbury’s “Slow Lane” checkout programme. Neither of these is a complete concept redesign; they are bolt-on accommodations within mainstream store formats. Sankalp Fresh would be the first ground-up elderly-centric grocery concept in a major emerging market.

Step 3: Define the Goal

Design a supermarket experience that makes adults aged 60 to 75 feel physically comfortable, cognitively at ease, and socially connected during their grocery shopping, such that they actively prefer Sankalp Fresh over all alternatives and visit more often than they would otherwise. The measurable outcome is a Net Promoter Score of 70 or above within 18 months of launch, an average basket size of Rs 1,800 per visit (nearly double the modern trade average of Rs 950), and a 30-day member retention rate of 65 percent or above.

This goal serves two equally important purposes. For the customer, it delivers dignity, convenience, and connection. For the business, it creates a defensible loyalty flywheel: elderly shoppers who feel genuinely respected do not switch, they recruit their peers, and they spend more per visit because they are not rushing out of discomfort. A 1 percent improvement in 30-day retention among Gold members translates directly to an estimated Rs 4.2 lakhs in additional annualized revenue per store at the target visit frequency.

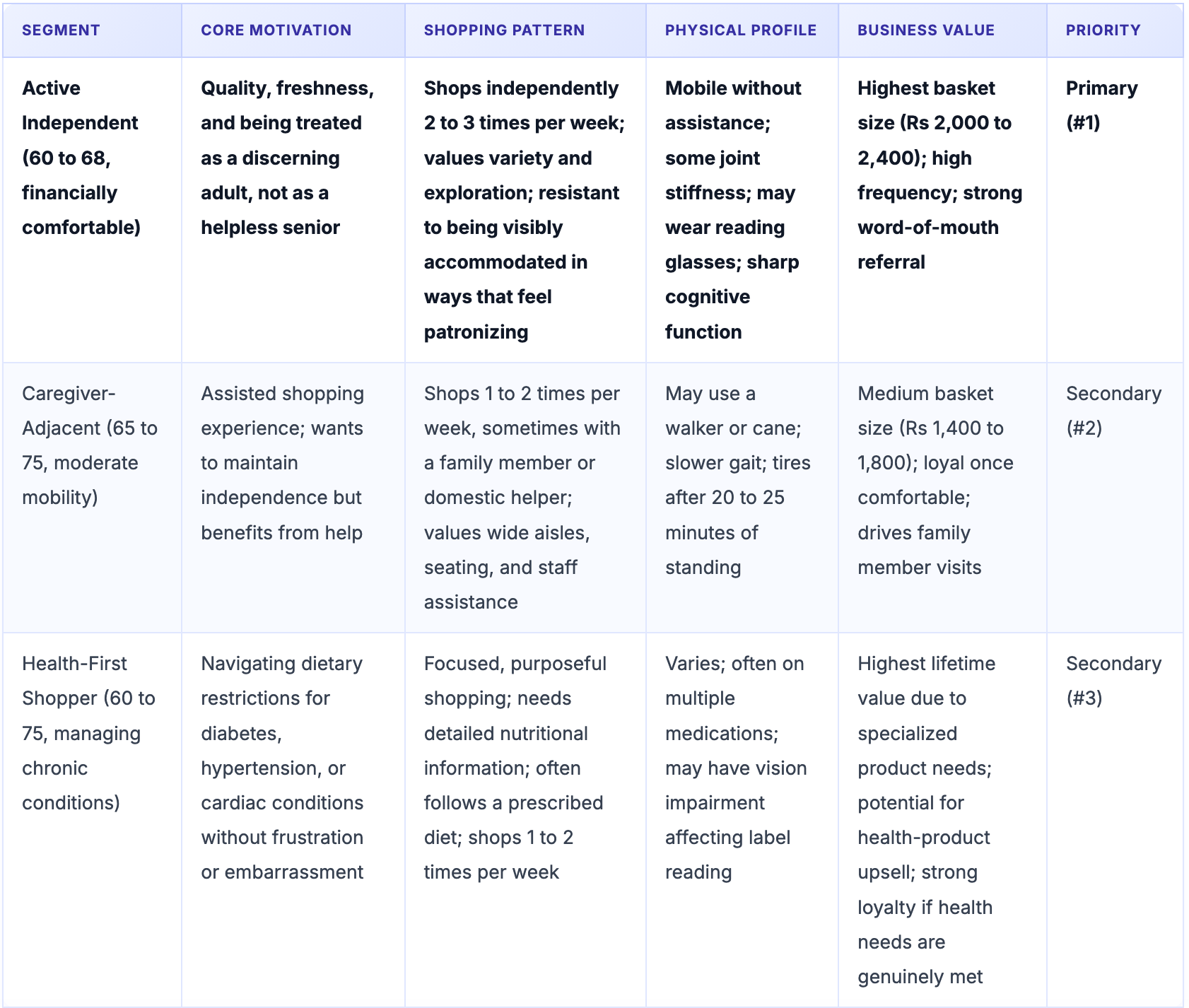

Step 4: User Segmentation

Within the 60 to 75 age band, the elderly grocery shopper is not a monolith. Shopping behavior, physical capability, social motivation, and digital fluency vary significantly. I identify three distinct sub-segments.

Prioritized segment: Active Independents.

The reason is both financial and strategic. Active Independents have the highest basket size and visit frequency, and they are the most likely to drive word-of-mouth referral among their peer networks. But more importantly, designing well for them is the hardest design challenge: they do not want to be treated as elderly. They want to be treated as discerning adults who happen to be 65. A store that gets this right for the Active Independent will automatically be usable and comfortable for the other two segments. The reverse is not true: designing primarily for the Caregiver-Adjacent segment would produce a store that feels like a medical facility, which would repel the Active Independent completely.

Representative Persona: Meera Krishnamurthy, 67, retired professor, Bengaluru Koramangala. Shops at Reliance Smart on Tuesday and Friday mornings. Stopped going on Saturday mornings after a bad experience in a long checkout queue. Spends approximately Rs 2,100 per visit. Cannot read the 6-point font on product labels without her phone camera. Gets physically uncomfortable after 40 minutes on hard floors. Does not use apps for shopping. Knows exactly which products she wants but sometimes cannot find them because the store layout changes with every new promotion cycle. She refers to Big Bazaar as “that noisy circus.” She would pay a Rs 299 monthly membership fee for a store that felt like it was designed for her.